Term Life vs. Whole Life Insurance: What’s the Difference?

Term Life vs. Whole Life Insurance: What’s the Difference?

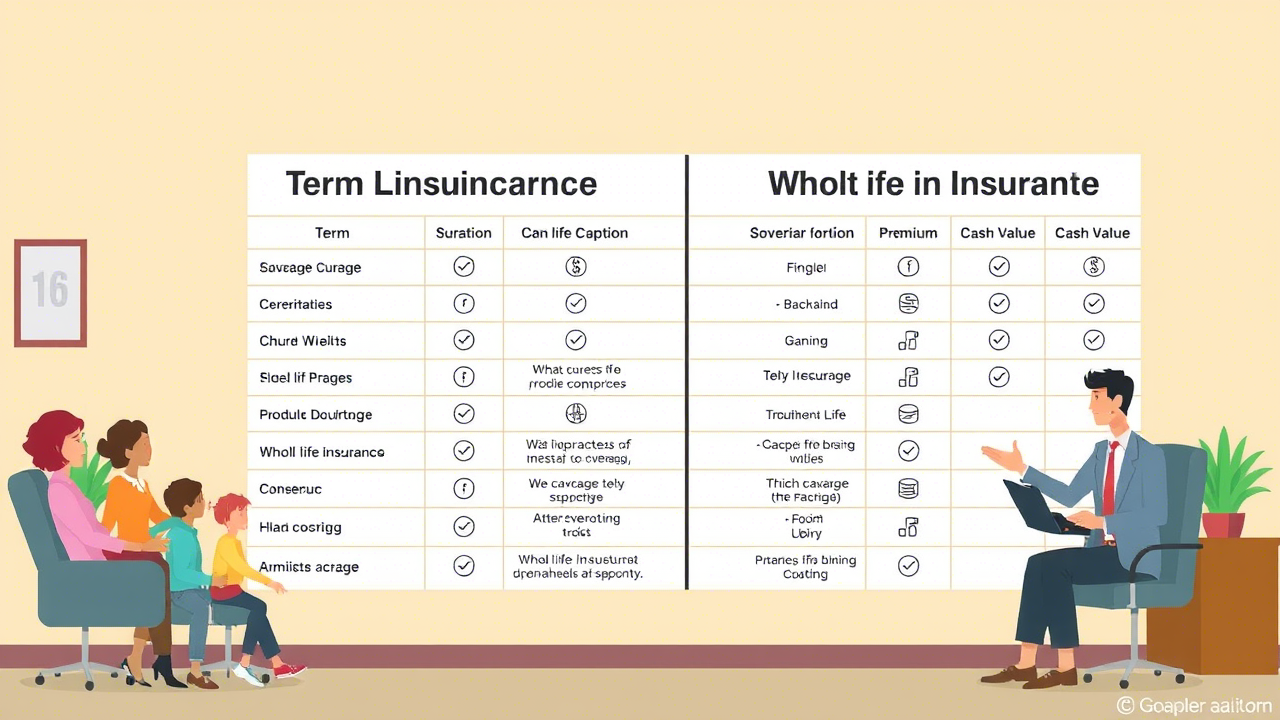

When it comes to choosing life insurance, many people find themselves weighing the differences between term life and whole life insurance. Both serve the primary purpose of providing financial security for loved ones, but they differ in structure, benefits, and cost. Understanding these differences can help you determine which policy best suits your needs.

What Is Term Life Insurance?

Term life insurance is a straightforward, temporary form of coverage that lasts for a predetermined period—commonly 10, 20, or 30 years. If the policyholder passes away during the term, the beneficiaries receive the death benefit. However, if the term expires and the policyholder is still alive, the coverage ends unless renewed or converted into a permanent policy.

Key Features of Term Life Insurance:

- Affordability – Generally, term life insurance premiums are lower than whole life premiums, making it an attractive option for individuals on a budget.

- Fixed Terms – The policy covers a set period, meaning you only pay for coverage when you need it most, such as during your working years.

- No Cash Value – Unlike whole life insurance, term policies do not accumulate cash value; they serve purely as a death benefit.

- Renewable Options – Some policies offer the ability to renew or convert into permanent insurance, though at higher premiums.

What Is Whole Life Insurance?

Whole life insurance, also known as permanent life insurance, provides lifelong coverage as long as premiums are paid. It also includes a cash value component that grows over time, which can be borrowed against or even withdrawn under certain circumstances.

Key Features of Whole Life Insurance:

- Lifetime Coverage – Unlike term life insurance, whole life policies do not expire, ensuring that beneficiaries will receive a payout regardless of when the policyholder passes away.

- Cash Value Growth – A portion of each premium contributes to a cash value account, which grows at a guaranteed rate over time.

- Fixed Premiums – Payments remain consistent throughout the life of the policy, making it easier to budget long-term.

- Loan and Withdrawal Options – Policyholders can borrow against the accumulated cash value or withdraw funds for various financial needs.

Which One Is Right for You?

The choice between term and whole life insurance depends on your financial goals, budget, and personal circumstances:

- Term Life Insurance Might Be Best If:

- You need affordable coverage for a specific period (e.g., until children are financially independent or a mortgage is paid off).

- You prefer lower premiums with no additional investment component.

- You want flexibility to convert to a permanent policy later if needed.

- Whole Life Insurance Might Be Best If:

- You want lifelong coverage with a guaranteed payout for your beneficiaries.

- You are looking for a policy that builds cash value over time.

- You prefer predictable premiums and potential borrowing options in the future.

Final Thoughts

Choosing between term and whole life insurance is a personal decision that depends on your financial goals and current situation. Term life insurance offers affordable, temporary coverage, while whole life insurance provides lifetime security with a savings component. Carefully evaluating your needs and speaking with a financial advisor can help ensure you select the best policy for you and your family’s future.